Brazil and Argentina: US trade tariffs on the doorstep

Steel and aluminium tariffs back on the table

Up until today, Argentina and Brazil have been outside the scope of the trade tensions with the USA. However, at the beginning of the month, Trump threatened to restore tariffs on Argentine and Brazilian steel and aluminium products. Last year, Trump imposed steel and aluminium tariffs on countries exporting steel and aluminium to the USA. Argentina and Brazil were exempt from the tariffs of 25% and 10% respectively as they subjected themselves to voluntary export quotas. However, this month Trump designated both countries as currency manipulators and threatened to levy the tariffs.

Little impact on the Brazilian and Argentine economy

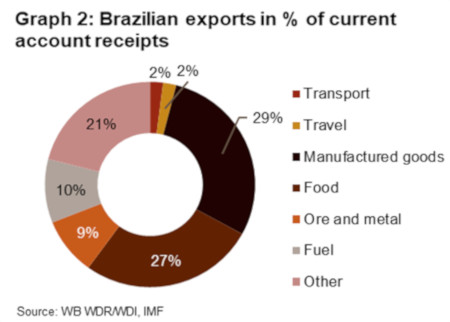

The tariffs will not have much impact on the economy as a whole, as the steel sector is a very small source of export revenue for both countries. In Argentina, ore and metal exports are almost insignificant at 0.4% of export revenue. Furthermore, iron and steel exports to the USA represent just 4% of their iron and steel exports. The impact will be more significant for Brazil. In Brazil, ore and metal comprises almost a tenth of export revenue. However, steel barely accounts for 2% of current account revenue while iron ore accounts for almost 8%. Hence, despite the USA representing about 34% of Brazil’s iron and steel exports, the impact of the steel and aluminium tariffs is expected to be contained for the Brazilian economy as well.

Are Brazil and Argentina currency manipulators?

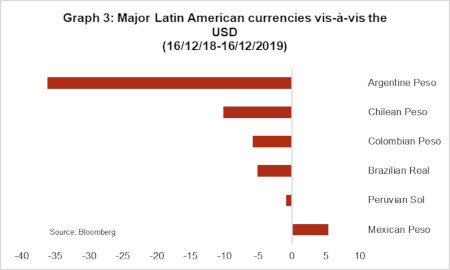

Since last year, Argentina and Brazil have seen their currencies depreciate in line with most major Latin American countries (see graph 3). The unrest in multiple Latin American countries in recent months (e.g. Chile and Colombia) is one of the main reasons Latin American countries are seeing their currency come under pressure. For Brazil and Argentina, domestic issues are at play too.

The Argentine peso was last year’s worst performing emerging market currency and is likely to retain its ranking in 2019. This is mainly due to two currency runs in two years. The first currency run in 2018 was the result of large macro-economic imbalances. The wide fiscal deficit, high inflation and high external debt vis-à-vis current account receipts in combination with an extreme drought hitting soybean exports led to panic in the financial markets. The run on the currency only halted thanks to the record IMF bailout with unpopular fiscal consolidation attached. The second currency crisis started in August 2019 when it became clear that the next President of Argentina was likely to be the leftist populist Alberto Fernández. Possible unorthodox or very distortive economic policies from a government led by Fernández, a potential large haircut on the high public debt (projected at 93% of GDP in 2019) and high demand among Argentinians for the USD put severe pressure on the currency. Only the imposition of currency controls slowed the rate of depreciation. However, as policy uncertainty remains after the inauguration of President Fernández, pressure on the currency is continuing.

The Brazilian real is a free-floating currency with occasional central bank interventions to avoid disruptive movements. The main reason for the (relatively small) depreciation in the past year is the implementation of a more accommodative monetary policy. As inflation is fairly low in the country (around 3.5% in 2019), and real GDP growth is quite sluggish (barely 1% expected in 2019), lowering the interest rate could lead to higher credit demand and boost the economy. Furthermore, political unrest in Latin American countries has led Brazil to pause its fiscal reforms for fear of fuelling domestic unrest. However, fiscal consolidation is necessary in the light of its high public debt (estimated at around 92% of GDP in 2019), making financial markets nervous and putting pressure on the real.

Hence, Brazil is not manipulating its currency, while the measures taken in Argentina were aimed at increasing the value of the peso. Furthermore, the tariff threats could put even more pressure on their exchange rates.

Why are these countries facing the ire of Trump?

Brazil and Argentina have long been outside the scope of Trump’s trade war. The main reason is that both countries have a trade deficit with the USA. Indeed, they import more from the USA than they export: an important indicator for Trump. However, the reason for Trump’s discontent can be found in soybean.

The USA was previously the world’s biggest soybean exporter, while China is the biggest importer. The trade war between the USA and China has led China to replace its soybean imports from the USA with imports from Brazil and, to a lesser extent, from Argentina. Brazil saw its soybean exports rise by 90% between 2016 and 2018. Brazil is also poised to overtake the USA to become the biggest soybean exporter this year. Nonetheless, a potential trade deal between the USA and China is likely to include higher soybean exports from the USA to China and could lead to lower Brazilian and Argentine exports in the future.

Therefore, the threats of tariffs on steel and aluminium could be a way to put pressure on Brazil and Argentina to rethink their soybean exports to China. Moreover, the USA’s moves also suggest that relations with Brazil are not a priority and relations with Argentina will become frostier following the election of Fernández as President.

Outlook for Argentina and Brazil

The outlook for Argentina and Brazil has not changed due to the tariff threats as they will not have much impact on the economy as a whole.

The outlook for the ST (2/7) and MLT political risk categories (5/7) is stable for Brazil. That being said, the poor state of public finances remains the Achilles heel. Brazil passed a landmark pension reform in 2019 to tackle its wide public deficit (predicted to be -7.5% of GDP in 2019). Although it is an important step, further reforms are necessary as public debt is expected to swell in the coming years. The focus is likely to shift to overhauling Brazil’s tax system, which is one of the most complex in the world. Nonetheless, pushing new fiscal reforms will not be a walk in the park. Another downside risk for Brazil is the Amazon fires. The (perceived) lack of reaction to these fires could scare away FDI (an important source of financing for Brazil’s small current account deficit) and put pressure on trade deals.

In Argentina, President Fernández’s new cabinet is facing a difficult time as it is negotiating with private debt bondholders and the IMF to put public debt on a more sustainable level. Furthermore, the government is trying to both tackle the fiscal deficit and revive the country’s economy. Argentina is experiencing its worst recession in a decade (around -3.1% is predicted in 2019), very high inflation (around 60%), a high level of public debt and falling foreign exchange reserves (still standing at an adequate 5 months of import cover in October 2019). In response, Fernández’s government has raised taxes on exports of agricultural products and put in place a 30% tax on all purchases made abroad last weekend. These measures could lead to hoarding in the agriculture sector and – more generally – fuel social and political tensions. The possibility of unorthodox economic policies (e.g. more stringent currency controls as well as price controls) or a depletion of foreign exchange reserves keep our outlook for both the ST and MLT political risk categories (6/7) tilted to the downside.

Analyst: Jolyn Debuysscher – J.Debuysscher@credendo.com