Short-term political risk: Cameroon, Madagascar, Papua New Guinea, Tunisia, Ukraine, Uzbekistan and Zambia

In the framework of its regular review of short-term (ST) political risk classifications, Credendo has upgraded nine countries (Bhutan, Greece, Kuwait, Madagascar, Papua New Guinea, Timor-Leste, Ukraine and Uzbekistan) and downgraded five countries (Antigua and Barbuda, Cameroon, Haiti, Tunisia and Zambia).

Cameroon: downgrade from 4/7 to 5/7

On the back of a sharply deteriorated short-term payment experience, Cameroon has been downgraded from category 4 to 5, that is, the category of most of its CEMAC peers. The CEMAC region is going through a crisis, marked by very low regional liquidity levels and uncertainty on the currency’s future stability. New exchange regulations were introduced to bring relief to the pooled foreign exchange reserves in the longer term but they have placed local banks under closer administrative scrutiny and have increased their workload, leading to (temporary) payment delays. As commercial banks will gradually get accustomed to the updated financial infrastructure and requirements, delays are most likely to diminish. Moreover Cameroon depends on IMF and donor support to cover financing gaps on its balance of payments although its current account deficit reached 3.7% of GDP in 2018 and is set to marginally moderate this year. The detrimental security situation in the anglophone regions is affecting national economic activity and export revenues, as they are vital productive regions (oil, cocoa and coffee).

Madagascar: upgrade from 5/7 to 4/7

Madagascar’s current account deficit remains confined (about -2% of GDP expected in 2019), although it is projected to widen due to higher investment-related imports, largely financed by increased external public borrowing. Gross foreign exchange reserves reached a healthy 3.5 months of import cover in May 2019 and are likely to gradually expand over the coming years. Even more important, the political situation has stabilised since the December 2018 election of President Rajoelina, followed by the successful legislative elections held in May 2019 that gave the president a legislative majority to work with. The new political reality seems to be generally accepted, lowering the risk of political unrest after decades of political instability and violence. Still, Madagascar remains a fragile state reliant on donor support and on a limited export base (vanilla, tourism and private transfers), and marked by widespread poverty and high exposure to natural disasters (Indian Ocean’s cyclone belt).

Papua New Guinea: upgrade from 5/7 to 4/7

The foreign exchange rationing – resulting from the authorities’ policy of keeping the kina overvalued – has sharply declined over the past year as mentioned in a recent publication. Although payment delays remain (with priority given to resource-related and staple imports), this positive development motivated Credendo to upgrade the country’s short term political risk to 4/7.

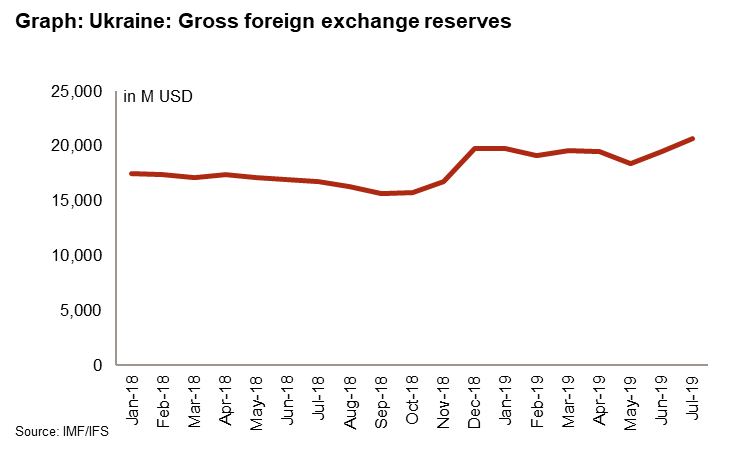

Ukraine: upgrade from 5/7 to 4/7

Following the presidential and parliamentary elections, political uncertainty has decreased. Indeed, the newly created party of President Zelensky (Servant of the People) won the majority of the seats in parliament. On the one side, the appointment of technocrats and former ministers in the newly formed government shows the willingness of the authorities to move forward with reforms such as the anti-corruption reform. On the other side, if it is confirmed that the government wants to reach an agreement with the former owner of PrivatBank, its relation with the IMF and its western backers could be jeopardised. In this context, Credendo upgraded it short-term political risk to category 4/7 to reflect the liquidity improvement. Indeed, the gross foreign exchange reserves have increased (cf. graph) while the short-term external debt and current account balance remain relatively stable.

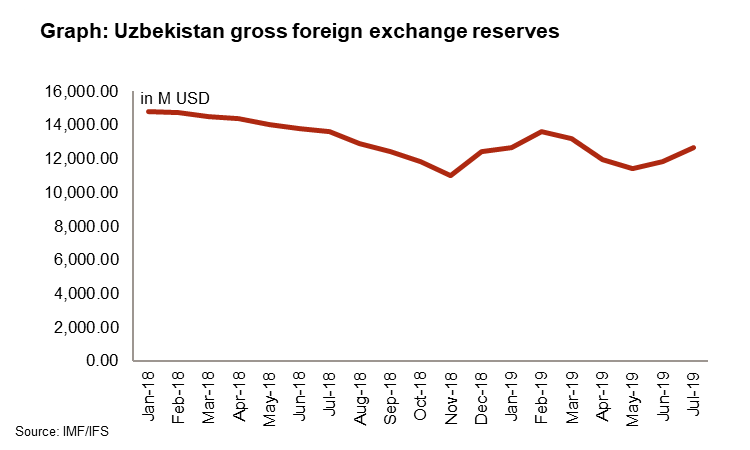

Uzbekistan: upgrade from 4/7 to 3/7

The ambitious economic reforms undertaken by current President Shavkat Mirziyoyev are underway. One aspect of his reform plan was to improve the quality and transparency of macroeconomic data. As a result, the figures of Uzbekistan’s gross foreign exchange reserves are now published by the IMF in its International Financial Statistics (IFS). These newly published figures (cf. graph below) show that gross foreign exchange reserves (excluding gold) cover about six months of imports, a comfortable level that led Credendo to upgrade its short-term political risk to category 3/7. This classification reflects the liquidity of a country. That being said, reforms also have pitfalls. Among other things, the liberalisation of the exchange rate and of the trade regime in 2017, along with the large credit growth, led to a sharp deterioration of the current account balance. Indeed, while the country posted a current account surplus of 2.5% of GDP in 2017, the balance turned into a deficit of about 7% of GDP in 2018 and is likely to remain in deficit this year. Looking ahead, the deterioration of the external balance – partly driven by a large credit expansion – is a factor to watch, as it could lead to a weakening of the liquidity and a boom-and-bust scenario.

Tunisia: downgrade from 4/7 to 5/7

Tunisia’s liquidity situation has been steadily deteriorating for some time now. This is caused mainly by the persistently large current account deficit, which amounted to around 11% of GDP at the end of 2018 and it is expected to remain at around 10% of GDP in 2019. As Tunisia is an oil-importing country, the higher oil prices in 2018 were a driver of the larger current account deficit. At the same time, Tunisia’s debt service keeps increasing. It is currently projected that the country will spend almost 20% of its current account receipts on servicing its external debt, which is a relatively high share and a strong increase compared to three years ago when it spent only 9.5%. The short-term external debt level in 2019 also remains at a medium/high level, at 35.1% of current account receipts. Last, gross foreign exchange reserves remain under pressure, as at beginning of 2019 they covered only a relatively low 2.6 months of imports. As all these elements lead to a deterioration of the liquidity position, it was decided to downgrade Tunisia’s short-term political risk to category 5/7.

Zambia: downgrade from 5/7 to 6/7

Zambia’s liquidity situation has deteriorated and is set to further erode in 2020. The country is confronted with extensive external financial needs following four years of outsized external borrowing. The downward trend in foreign exchange reserves is expected to continue due to large financing gaps on the balance of payments projected in the coming years. As a result, the import cover reached a 15-year low (1.3 months) in June 2019. Indeed, capital outflows have increased drastically as investors are pulling out while the copper sector is confronted with severe tax increases and government seizure attempts, plummeting export returns. A government debt default is in the cards with accumulating domestic arrears, a 2019 budget deficit set to reach 9% of GDP again (10.7% in 2018) and the unsustainable borrowing plans for a series of debt-financed infrastructure projects being maintained nonetheless. Due to erratic policy decisions made by the internationally and domestically contested government of President Lungu, an IMF programme to help face the financial crisis remains unlikely to be concluded. As a consequence, Zambia’s short-term political risk classification has been downgraded to 6/7.