West African Economic and Monetary Union: Despite strong economic growth performance, the risks confronting the WAEMU are rife

The WAEMU as part of the CFA franc zone

The CFA franc zone includes 14 Sub-Saharan African countries (and the Comoros), divided among the Central African Economic and Monetary Community (CEMAC) and the West African Economic and Monetary Union (WAEMU). The CFA franc refers to two currencies (XOF and XAF) that are at parity and have always had the same monetary value against other currencies. The CFA franc was anchored to the French franc until January 1999, after which the euro became the anchor currency. It was devalued in 1948 and 1960 and the last (sharp) devaluation was in 1994, after which today’s peg of 655.96 CFA francs to 1 euro was set. The monetary cooperation with France is based on four principles: an unlimited convertibility guarantee from the French Treasury, fixed parities, free transferability inside the region and pooled foreign exchange reserves (at the Central Bank of West African States (BCEAO) and the Bank of Central African States (BEAC)).

Consequently, the risk of non-payment in a trade transaction caused by transfer issues or foreign exchange shortages has been mitigated for members of the monetary arrangement. This is reflected in Credendo’s maximum short-term political risk classification of category 5/7 for the CFA countries1. Moreover, the peg to the euro and the prohibition on monetising fiscal deficits have kept inflation low (around 3%), in contrast with the rest of Sub-Saharan Africa.

WAEMU member countries and their common features

The WAEMU comprises Côte d’Ivoire, Senegal, Mali, Burkina Faso, Benin, Niger, Togo and Guinea-Bissau, listed in order of GDP magnitude (high to low). All members are net oil importers and some are rather fragile (small export bases) and politically unstable. Their high reliance on one or two export goods exposes members to terms of trade shocks. Trade flows are particularly dependent on commodities like cocoa (Côte d’Ivoire), cotton (Burkina Faso, Benin), gold (Mali, Burkina Faso), uranium (Niger) and phosphates (Togo). The potential for regional trade integration should be further deepened as trade within the WAEMU reaches just 10% of total trade flows, notwithstanding the single currency and the absence of tariff barriers. Moreover, the inflow of international investments remains limited despite the absence of foreign exchange risks, probably due to a lack of infrastructure and poor institutions. Today’s high reliance on the public sector should be addressed by improving competitiveness and unlocking private-sector-led growth, which are essential for durable economic progress and sustainable public finances.

Elevated economic growth and large public investments

The WAEMU has been one of the fastest-growing regions in Sub-Saharan Africa since 2011. Average real GDP growth projections remain upbeat at between 6% and 7% at least for another 5 years, while most members are set to grow more than 5% per year. Rising household consumption – especially following the end of civil conflict in Côte d’Ivoire – and large public investments in infrastructure projects have driven growth. Indeed, WAEMU domestic investment growth has been particularly strong in recent years, reaching an average of 23.4% of GDP in 2018. However, with relatively low national savings rates (16.5% of GDP in 2018), investments are largely financed externally, leading to substantial external and fiscal imbalances. The overall regional fiscal deficit has been on the rise and reached 4.4% and 4.3% of GDP respectively in 2016 and 2017. Accordingly, public debt increased from 36% of GDP in 2012 to 52% in 2018, with a growing proportion held externally. Thanks to consolidation efforts, the fiscal deficit narrowed to 3.8% of GDP in 2018 and should reach the WAEMU’s 3% of GDP target by the end of 2019, smoothing public debt accumulation.

Credendo’s assessment of the WAEMU’s liquidity

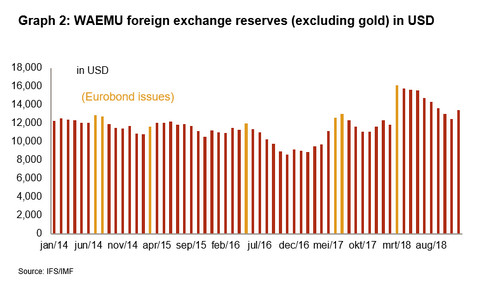

The foreign exchange reserves buffer held at the BCEAO was lowered following the tumble of commodity prices and spreading security issues in the Sahel from 6 months of import cover in 2011 to about 4.7 months by the end of 2014, which is a relatively low level for defending the currency peg. As displayed in graph 2, reserves came under additional pressure in 2016, falling to 3.9 months of import cover, as large infrastructure investments require substantial capital-goods imports, raising the current account deficit. In 2018, the regional current account deficit widened to a record 6.8% of GDP but is projected to move back towards 5% in the coming years (partly thanks to new oil and gas production in Senegal). Deficits have been largely financed by international donor support, concessional financing and foreign direct investments, yet non-concessional external borrowing has been on the rise, especially in Senegal, Côte d’Ivoire and Benin. As a result, the burden of servicing public debts increased from an average of 20.8% of government revenues in 2015 to 33% in 2018. Benin, Togo and Senegal carried the highest debt servicing burden in 2018. Since 2017, liquidity pressure has been eased by large Eurobond issuances by Senegal and Côte d’Ivoire on the one hand, and better enforcement of export receipt repatriation requirements on the other. As a result, foreign exchange reserves reached 4.3 months of import cover again at the end of 2018. Essential reforms in the banking sector were implemented in 2018 to meet new solvency requirements and help banks to deal with considerable concentration, credit and liquidity risks.

Credendo’s regional outlook and identified risks

There have been concerns over CFA franc stability since the drop in international oil prices shrunk the liquidity levels of the oil-dependent CEMAC economies, raising fears of devaluation. Since 2016, the IMF has been coordinating regional stabilisation efforts. Together with the assurance of international support for the current peg, monetary and fiscal reforms have decelerated devaluation fears. Nevertheless, the fast conclusion of an IMF programme for Equatorial Guinea and the Republic of the Congo will be essential for the CEMAC’s liquidity position to recover. The liquidity crisis could pose a monetary risk to the WAEMU (capital outflows), even though the two unions essentially function independently.

WAEMU GDP growth projections are positive and the liquidity buffer should gradually rebuild if fiscal consolidation efforts are maintained. However, a deterioration of the security situation in Burkina Faso, Mali or Niger could derail forecasts, while political instability in Guinea-Bissau and Togo continues to be a leading risk factor. The tense 2020 presidential election in Côte d’Ivoire is another important event to monitor. Insufficient economic inclusiveness could nurture social instability as poverty remains rampant in the region. Moreover, adverse terms of trade shocks and banking sector vulnerabilities pose noteworthy risks. The WAEMU’s exposure to global financial markets has increased since the Eurobond issuances. Therefore, the region also got exposed to financial market shocks (capital outflows, reversed risk appetite) and rising global interest rates, which could increase financing costs.

The plan to merge with the other members of the Economic Community of West African States (ECOWAS) (The Gambia, Ghana, Guinea, Liberia, Nigeria and Sierra Leone) into a regional monetary union with a single currency (the “eco”) was established in 1999 but has been confronted with numerous obstacles and setbacks over the years. Such a common currency creates important opportunities when it comes to regional trade and continental (economic) influence, but conditions to exploit these merits remain problematic (weak infrastructure, informal trade, security risks, lacking macro-economic stability and debt sustainability). Therefore, the chances of the “eco” being launched on the newly set deadline of January 2020 are very slim. To date, the WAEMU has never presented a plan for how it would dissolve the CFA franc to join the “eco”. Members could delay participation further, being unwilling to risk losing the backing of the French Treasury and the general macro-economic stability provided by CFA zone membership.

Analyst: Louise Van Cauwenbergh – l.vancauwenbergh@credendo.com

1 Not applied when a high risk of war justifies a higher rating.